-

×

Momentum Explained. Vol.1

1 × $6.00

Momentum Explained. Vol.1

1 × $6.00 -

×

MQ MZT with Base Camp Trading

1 × $31.00

MQ MZT with Base Camp Trading

1 × $31.00 -

×

Hot Commodities: How Anyone Can Invest Profitably in the World's Best Market with Jim Rogers

1 × $6.00

Hot Commodities: How Anyone Can Invest Profitably in the World's Best Market with Jim Rogers

1 × $6.00 -

×

The Fortune Strategy. An Instruction Manual

1 × $6.00

The Fortune Strategy. An Instruction Manual

1 × $6.00 -

×

Trading Options for Dummies with George Fontanills

1 × $6.00

Trading Options for Dummies with George Fontanills

1 × $6.00 -

×

Forex Strategies Course For Weekly Charts with Cory Mitchell - Vantage Point Trading

1 × $4.00

Forex Strategies Course For Weekly Charts with Cory Mitchell - Vantage Point Trading

1 × $4.00 -

×

Ninja Order Flow Trader (NOFT)

1 × $39.00

Ninja Order Flow Trader (NOFT)

1 × $39.00 -

×

The Volatility Course Workbook: Step-by-Step Exercises to Help You Master The Volatility Course - George Fontanills & Tom Gentile

1 × $6.00

The Volatility Course Workbook: Step-by-Step Exercises to Help You Master The Volatility Course - George Fontanills & Tom Gentile

1 × $6.00 -

×

Expectations Investing with Alfred Rappaport

1 × $6.00

Expectations Investing with Alfred Rappaport

1 × $6.00 -

×

Read the Greed – LIVE!: Vol. II with Mike Reed

1 × $6.00

Read the Greed – LIVE!: Vol. II with Mike Reed

1 × $6.00 -

×

The Option Trader’s Handbook (2008) with Jeff Augen

1 × $6.00

The Option Trader’s Handbook (2008) with Jeff Augen

1 × $6.00 -

×

Using Options to Buy Stocks: Build Wealth with Little Risk and No Capital - Dennis Eisen

1 × $4.00

Using Options to Buy Stocks: Build Wealth with Little Risk and No Capital - Dennis Eisen

1 × $4.00 -

×

W.D. Gann’s Best Trading Systems with Myles Wilson-Walker

1 × $27.00

W.D. Gann’s Best Trading Systems with Myles Wilson-Walker

1 × $27.00 -

×

Trading Mastery Course 2009

1 × $6.00

Trading Mastery Course 2009

1 × $6.00 -

×

Don Fishback ODDS The Key to 95 Winners

1 × $6.00

Don Fishback ODDS The Key to 95 Winners

1 × $6.00 -

×

Automatic Millionaire (Audio Book) with David Bach

1 × $6.00

Automatic Millionaire (Audio Book) with David Bach

1 × $6.00 -

×

The Multi-Fractal Markets Educational Course with Dylan Forexia

1 × $39.00

The Multi-Fractal Markets Educational Course with Dylan Forexia

1 × $39.00 -

×

JeaFx 2023 with James Allen

1 × $5.00

JeaFx 2023 with James Allen

1 × $5.00 -

×

The Bollinger Bands Swing Trading System 2004 with Larry Connors

1 × $6.00

The Bollinger Bands Swing Trading System 2004 with Larry Connors

1 × $6.00 -

×

The Forex Chartist Companion: A Visual Approach to Technical Analysis with Michael Duane

1 × $6.00

The Forex Chartist Companion: A Visual Approach to Technical Analysis with Michael Duane

1 × $6.00 -

×

CNBC 24-7 Trading with Barbara Rockefeller

1 × $6.00

CNBC 24-7 Trading with Barbara Rockefeller

1 × $6.00 -

×

Pro Trend Trader 2017 with James Orr

1 × $31.00

Pro Trend Trader 2017 with James Orr

1 × $31.00 -

×

The Options Handbook with Bernie Schaeffer

1 × $6.00

The Options Handbook with Bernie Schaeffer

1 × $6.00 -

×

Philadelphia Seminar Replay & PDF Study Guide with ASFX Day Trading

1 × $31.00

Philadelphia Seminar Replay & PDF Study Guide with ASFX Day Trading

1 × $31.00 -

×

Astro FX 2.0

1 × $6.00

Astro FX 2.0

1 × $6.00 -

×

The Unified Theory of Markets with Earik Beann

1 × $78.00

The Unified Theory of Markets with Earik Beann

1 × $78.00 -

×

Trading Breakouts with Options By Keith Harwood - Option Pit

1 × $23.00

Trading Breakouts with Options By Keith Harwood - Option Pit

1 × $23.00 -

×

Trading the Eclipses

1 × $6.00

Trading the Eclipses

1 × $6.00 -

×

Mission Million Money Management Course

1 × $31.00

Mission Million Money Management Course

1 × $31.00 -

×

Dow Theory Redux with Michael Sheimo

1 × $6.00

Dow Theory Redux with Michael Sheimo

1 × $6.00 -

×

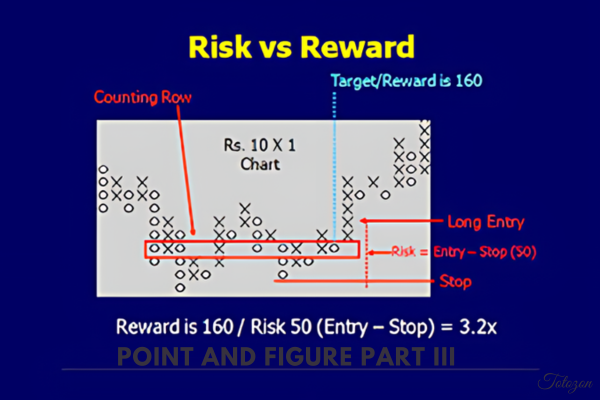

Point And Figure Part III By Bruce Fraser & Roman Bogomazov - Wyckoff Analytics

1 × $23.00

Point And Figure Part III By Bruce Fraser & Roman Bogomazov - Wyckoff Analytics

1 × $23.00 -

×

NFTMastermind with Charting Wizards

1 × $5.00

NFTMastermind with Charting Wizards

1 × $5.00 -

×

Training Program

1 × $15.00

Training Program

1 × $15.00 -

×

AnswerStock with Timothy Sykes

1 × $5.00

AnswerStock with Timothy Sykes

1 × $5.00 -

×

Learn About Trading Options From a Real Wallstreet Trader with Corey Halliday & Todd parker

1 × $6.00

Learn About Trading Options From a Real Wallstreet Trader with Corey Halliday & Todd parker

1 × $6.00 -

×

Characteristics and Risks of Standardized Options

1 × $6.00

Characteristics and Risks of Standardized Options

1 × $6.00 -

×

Mind of a Trader with Alpesh Patel

1 × $6.00

Mind of a Trader with Alpesh Patel

1 × $6.00 -

×

Making The Leap Learning To Trade With Robots with Scott Welsh

1 × $15.00

Making The Leap Learning To Trade With Robots with Scott Welsh

1 × $15.00 -

×

Low Timeframe Supply and Demand with SMC Gelo

1 × $5.00

Low Timeframe Supply and Demand with SMC Gelo

1 × $5.00 -

×

Warrior Trading: Inside the Mind of an Elite Currency Trader with Clifford Bennett

1 × $6.00

Warrior Trading: Inside the Mind of an Elite Currency Trader with Clifford Bennett

1 × $6.00 -

×

Best of the Best: Collars with Amy Meissner & Scott Ruble

1 × $15.00

Best of the Best: Collars with Amy Meissner & Scott Ruble

1 × $15.00 -

×

VXX Made Easy By Option Pit

1 × $62.00

-

×

Drewize Banks Course

1 × $5.00

Drewize Banks Course

1 × $5.00 -

×

Trading the Ross Hook (tradingeducators.com)

1 × $6.00

Trading the Ross Hook (tradingeducators.com)

1 × $6.00 -

×

Trading Psychology - How to Think Like a Professional Trader - 4 DVD

1 × $6.00

Trading Psychology - How to Think Like a Professional Trader - 4 DVD

1 × $6.00 -

×

The Essays of Waren Buffet. Lessons for Corporate America with Lawrence A.Cunningham

1 × $6.00

The Essays of Waren Buffet. Lessons for Corporate America with Lawrence A.Cunningham

1 × $6.00 -

×

Wifxa - INSTITUTIONAL SCALPING

1 × $23.00

Wifxa - INSTITUTIONAL SCALPING

1 × $23.00 -

×

Perfect Strategy - SPX Daily Options Income with Peter Titus - Marwood Research

1 × $15.00

Perfect Strategy - SPX Daily Options Income with Peter Titus - Marwood Research

1 × $15.00 -

×

VSTOPS ProTrader Strategy (Nov 2013)

1 × $6.00

VSTOPS ProTrader Strategy (Nov 2013)

1 × $6.00 -

×

A Process for Prudential Institutional Investment with Bancroft, Caldwell, McSweeny

1 × $6.00

A Process for Prudential Institutional Investment with Bancroft, Caldwell, McSweeny

1 × $6.00 -

×

Basic Astrotech

1 × $6.00

Basic Astrotech

1 × $6.00 -

×

Order flow self-study training program with iMFtracker

1 × $10.00

Order flow self-study training program with iMFtracker

1 × $10.00

Portfolio Management using Machine Learning: Hierarchical Risk Parity

Original price was: $599.00.$39.00Current price is: $39.00.

File Size: 161 MB

Delivery Time: 1–12 hours

Media Type: Online Course

Content Proof: Watch Here!

You may check content proof of “Portfolio Management using Machine Learning: Hierarchical Risk Parity” below:

Portfolio Management using Machine Learning: Hierarchical Risk Parity

In the realm of finance, where every decision holds weighty consequences, the integration of machine learning has revolutionized portfolio management. Among the innovative techniques, one stands out for its efficacy: Hierarchical Risk Parity (HRP). This method not only addresses traditional portfolio management challenges but also enhances risk management through the utilization of machine learning algorithms.

Understanding Portfolio Management

Defining Portfolio Management

Portfolio management involves the art and science of making decisions about investment mix and policy, matching investments to objectives, asset allocation, and balancing risk against performance.

Challenges in Traditional Portfolio Management

Traditional portfolio management faces challenges like lack of diversification, inefficient risk allocation, and difficulties in rebalancing portfolios.

The Emergence of Machine Learning in Finance

Integration of Machine Learning

Machine learning algorithms analyze vast amounts of data to identify patterns and make predictions, providing insights that enhance decision-making processes.

Advantages of Machine Learning in Portfolio Management

- Improved Decision Making: Machine learning algorithms can process data at a speed and scale that surpasses human capabilities, enabling more informed investment decisions.

- Enhanced Risk Management: Machine learning models can identify and assess risks more accurately, leading to better risk mitigation strategies.

- Increased Efficiency: Automation of repetitive tasks frees up time for portfolio managers to focus on strategic decision-making.

Hierarchical Risk Parity (HRP)

Understanding HRP

Hierarchical Risk Parity is a portfolio optimization technique that allocates risk across assets in a hierarchical structure. It aims to achieve better diversification and risk management by considering the covariance structure of assets.

Key Components of HRP

- Clustering: Assets are grouped into clusters based on their correlation.

- Hierarchical Structure: Clusters are arranged hierarchically, with higher-level clusters representing broader asset categories.

- Risk Parity Optimization: Risk is allocated within and across clusters to achieve parity, ensuring each asset contributes equally to the portfolio’s overall risk.

Benefits of HRP

- Improved Diversification: HRP allocates risk more evenly across assets, reducing concentration risk.

- Enhanced Risk Management: By considering the covariance structure, HRP identifies and mitigates systemic risks effectively.

- Adaptability: HRP can accommodate various asset classes and market conditions, making it a versatile tool for portfolio managers.

Implementing HRP with Machine Learning

Data Collection and Preprocessing

- Data Collection: Historical financial data for relevant assets is collected from various sources.

- Data Preprocessing: The data is cleaned, normalized, and transformed to make it suitable for analysis.

Model Training

- Feature Selection: Relevant features that influence asset returns and risk are identified.

- Algorithm Selection: Machine learning algorithms such as clustering algorithms and optimization techniques are chosen based on the nature of the problem.

- Model Training: The model is trained using historical data to learn patterns and relationships between assets.

Portfolio Construction and Optimization

- Asset Allocation: HRP is applied to allocate assets based on risk contributions.

- Portfolio Optimization: The portfolio is optimized to achieve desired risk-return characteristics while adhering to constraints such as investment objectives and regulatory requirements.

Conclusion

In conclusion, the integration of machine learning, particularly Hierarchical Risk Parity, has transformed portfolio management by enhancing diversification, risk management, and decision-making processes. By leveraging data-driven insights and advanced algorithms, portfolio managers can navigate complex market dynamics more effectively, ultimately maximizing returns while mitigating risks.

FAQs

1. What is the role of machine learning in portfolio management? Machine learning algorithms analyze data to identify patterns and make predictions, improving decision-making processes and risk management in portfolio management.

2. How does Hierarchical Risk Parity differ from traditional portfolio optimization techniques? Hierarchical Risk Parity considers the covariance structure of assets and allocates risk across clusters, resulting in better diversification and risk management compared to traditional techniques.

3. Can Hierarchical Risk Parity accommodate different types of assets? Yes, Hierarchical Risk Parity can accommodate various asset classes and market conditions, making it a versatile tool for portfolio managers.

4. What are the key benefits of implementing Hierarchical Risk Parity with machine learning? The benefits include improved diversification, enhanced risk management, and adaptability to different market conditions.

5. How does data preprocessing contribute to the effectiveness of HRP? Data preprocessing ensures that the input data is clean, normalized, and transformed, enabling accurate analysis and model training for Hierarchical Risk Parity.

Be the first to review “Portfolio Management using Machine Learning: Hierarchical Risk Parity”

You must be logged in to post a review.

Related products

Original price was: $310.00.$23.00Current price is: $23.00.

Original price was: $695.00.$41.00Current price is: $41.00.

Original price was: $497.00.$31.00Current price is: $31.00.

Forex Trading

Original price was: $2,000.00.$23.00Current price is: $23.00.

Original price was: $999.00.$5.00Current price is: $5.00.

Forex Trading

Original price was: $125.00.$17.00Current price is: $17.00.

Forex Trading

Original price was: $2,997.00.$23.00Current price is: $23.00.

Forex Trading

Original price was: $850.00.$23.00Current price is: $23.00.

Forex Trading

Original price was: $397.00.$31.00Current price is: $31.00.

Forex Trading

The Complete Guide to Multiple Time Frame Analysis & Reading Price Action with Aiman Almansoori

Original price was: $1,399.00.$13.00Current price is: $13.00.

Forex Trading

Original price was: $500.00.$5.00Current price is: $5.00.

Forex Trading

Original price was: $799.00.$15.00Current price is: $15.00.

Original price was: $497.00.$11.00Current price is: $11.00.

Forex Trading

Original price was: $1,098.00.$39.00Current price is: $39.00.

Original price was: $1,849.00.$15.00Current price is: $15.00.

Forex Trading

Original price was: $1,898.00.$10.00Current price is: $10.00.

Original price was: $895.00.$15.00Current price is: $15.00.

Forex Trading

Original price was: $697.00.$5.00Current price is: $5.00.

Original price was: $4,995.00.$15.00Current price is: $15.00.

Forex Trading

Original price was: $499.00.$15.00Current price is: $15.00.

Reviews

There are no reviews yet.